Global Macro Trading for Idiots: Part Three - Global Macro Trading for Idiots: Part Three

Short-Term Interest Rates

Hello, idiots.

If you thought yield curves and FX were fun, we’re about to go on a journey to the heart of global macro.

Short term interest rate (STIR) instruments add a whole new dimension to the excitement of “having opinions about what the Fed will do” (as we all know, people with opinions about what the Fed will do are some of the most interesting - and all very reserved about sharing these opinions with others).

In our previous installments, we covered the basics of trading the US yield curve and foreign exchange. By now, you should have a solid grasp on concepts like curve steepeners and flatteners (in both bonds and futures - steepener = long shorter maturity, short longer maturity and vice versa for flatteners), flies, why interest rate differentials matter so damn much in FX and the general fact that global macro is, in fact, the world’s greatest guessing game.

If you don’t, go to the remedial class and read the last two installments:

You may be noticing a theme in these pieces, something along the lines of…

Yield curves, FX interest rate differentials, equity indices..directly, indirectly or in some third way it can all seem like one big rates trade circlejerk.

So; today, we're going to simply bypass the middleman and go directly to the source - exploring how to trade these rate expectations using STIR futures, futures spreads and options. Then, we are going to take your newfound basic knowledge of STIR and absolutely manhandle it by talking about stuff like swaps and repo.

And you can know for sure this is 100% human authored because the AI doesn’t yet have the kind of brain damage nor mental illness necessary to express what it’s like to trade Euribors in words.

Still, this is Global Macro Trading for Idiots, not “for idiots, by idiots”. And while I can certainly punt midcurves efficiently, I needed someone who understood both memes and STIR well enough to bring this to the next level.

There’s a lot of stuff that’s beyond my realm in terms of IR Swaps, FX Swaps, Cross-Currency Basis etc. that I needed a real expert in…

And then I saw this:

Bingo.

I’m going to take you from “what’s a sofr” to “let’s put on the z4z5 steepener” and he will take you the rest of the way down the rabbit hole with an overview that features such nonsense words as “cross currency basis” and “covered interest rate parity.

It’s going to be really fun…interesting…STIRrific…

Okay, I’m not going to lie to you, you will hate both of us by the end of this article.

But at least you’ll have a solid foundation in short term interest rate trading. Provided that, when it comes to trading STIR, you’d currently self-describe as an idiot or some synonym thereof.

Because that's where "Global Macro Trading for Idiots" comes in.

Just be forewarned that we’ll be getting progressively less idiotic as the article goes on, thanks to the contributions of notorious non-idiot (in matters STIR related) Sir of Finance.

One more thing: normally I split the revenue generated from my articles with my collaborators. This is going out to everyone, free of charge, and because Sir of Finance is a gentleman (as the name infers),

We’ll be donating half of all subscription fees generated through this article to Doctor’s Without Borders. Unfortunately, there was no charity set up ready to accept donations for traders who have brain damage due to trading Euribors.

Upgrade to paid

Okay, with that said, let’s begin…

The (Very) Basics of STIR and STIR Futures

For the uninitiated, STIR futures are derivative contracts that allow traders to bet on the future direction of short-term interest rates, typically tied to interbank lending rates like or central bank policy rates. They're the purest way to express your view on what central bankers will do (or won't do) in the coming months and years. And if you really want to get fancy, you can even trade options on these futures to create all sorts payoff profiles.

But before we get into the nitty-gritty of cross-currency basis, DV01 and midcurves, let's take a step back and understand why anyone would even bother with these instruments in the first place. Since central banks are the puppet masters of the global economy, pulling the strings of interest rates to keep inflation in check or promote growth, macro traders spend pretty much all their time anticipating their next move and position accordingly.

STIR futures provide a liquid and efficient way to do just that. And not just that, but ways to do that with accuracy you just can’t get in other instruments.

If you think the ECB will be forced to cut rates into negative territory by the end of the year, you’re going to want to be doing something with Euribors if that’s the extent of your thesis.

The differential to SOFR won’t matter like it would with EURUSD, and it won’t matter whether it’s a policy mistake that leads to a massive rally in risk assets or it’s response to a previous policy mistake that put the EU in a massive, very-bearish-for-risk-assets recession (for believability the only certainty in this hypothetical is that of an ECB policy mistake).

Regardless of those confounding variables you’d have to deal with by expressing this thesis using other instruments, you’ll make money if you’re long December Euribor Futures (and a lot more money if you’ve got out of the money calls on them).

Maybe you think the market has gotten irrationally exuberant about the quantity of rate cuts the Fed will deliver in 2024? You can sell Z4 SOFR futures. In fact, you can sell some SOFR futures in December 2024 and buy some in December 2025 to isolate your trade to just rate expectations in 2025.

If you think the Bank of Japan will…nevermind actually we’re not going to talk about Japanese rates in this one. (I miss you, Kuroda).

The possibilities are truly (perhaps unfortunately) endless for expressing your unique view on what the economists decide. We’re going to go over some of the basics for doing that, but…

Before we get into it for real, you should be aware that trading STIR futures is not for the faint of heart. These markets are dominated by big banks, hedge funds, and other institutional players with deep pockets. They tend to act a lot differently than other asset classes.

You can go look at how SOFR futures react to headlines and data, unlike trading spoos the reaction in STIR sometimes tends to be much less something that can be described as “price action”. With some degree of regularity, it’s much more accurately described as “teleportation”.

Unlike equity index futures where your win condition is “market participants are currently wrong but eventually see the error of their ways and come around to my way of thinking”, STIR futures have an element of that but also the element of “then a bunch of economists decide whether you’re right or wrong, and sometimes you find out about this decision because one of the economists gets too chatty with the press” and other fun eccentricities.

Here are two examples, post Silicon Valley Bank collapse and the Nikileaks episode of 2022.

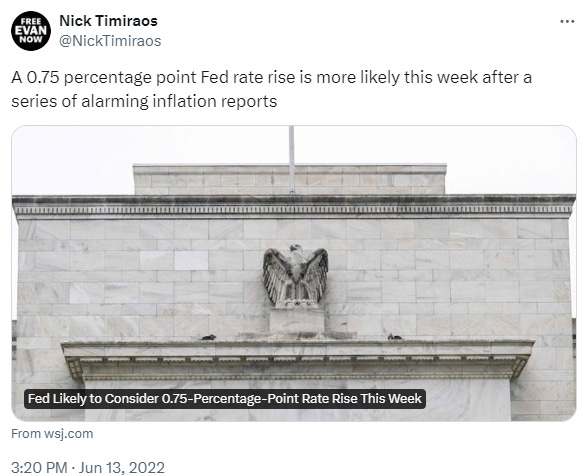

Even in significant selloffs in equity indices, there’s some level of liquidity, meanwhile sometimes what you get in STIR is a result that’s so unambiguous (this is the most extreme example of that, since it was literally a WSJ reporter telling the world the Fed would hike 75 and not 50) that between the current price and the correct price there will be zero bids (or zero offers if the scenario was reversed to deal with cuts).

Hence, “teleportation”, as you can see on the above chart showing the reaction of ES vs. SFRM22 to the tweet below from “Fed Whisperer” Nick Timiraos that earned him the nickname among STIR traders of “Nicky Leaks”. Whether that’s an affectionate nickname or one filled with pure hatred is a function of the individual STIR trader’s positioning exactly one second prior to the tweet:

That’s something that you’re going to want to keep in mind when you’re trading and assessing how much risk you’re taking. Obviously if you have a marketable stop order in on a position, you’re going to be facing some level of slippage or generally getting out at worse prices than you could have. If you have a stop order in a SOFR futures position and something like this happens, the only price you’re going to get out at is in the range of the newly-teleported-to correct one.

Now that you’re all sufficiently frightened by them, let’s get into the basics of trading STIR, beginning with how STIR futures work.

Hello, idiots.

If you thought yield curves and FX were fun, we’re about to go on a journey to the heart of global macro.

Short term interest rate (STIR) instruments add a whole new dimension to the excitement of “having opinions about what the Fed will do” (as we all know, people with opinions about what the Fed will do are some of the most interesting - and all very reserved about sharing these opinions with others).

In our previous installments, we covered the basics of trading the US yield curve and foreign exchange. By now, you should have a solid grasp on concepts like curve steepeners and flatteners (in both bonds and futures - steepener = long shorter maturity, short longer maturity and vice versa for flatteners), flies, why interest rate differentials matter so damn much in FX and the general fact that global macro is, in fact, the world’s greatest guessing game.

If you don’t, go to the remedial class and read the last two installments:

LINK: Global Macro Trading for Idiots: Trading the Yield Curve with Bond Futures

LINK: Global Macro Trading for Idiots: The Brain Damaging World of FX

You may be noticing a theme in these pieces, something along the lines of…

Yield curves, FX interest rate differentials, equity indices..directly, indirectly or in some third way it can all seem like one big rates trade circlejerk.

So; today, we're going to simply bypass the middleman and go directly to the source - exploring how to trade these rate expectations using STIR futures, futures spreads and options. Then, we are going to take your newfound basic knowledge of STIR and absolutely manhandle it by talking about stuff like swaps and repo.

And you can know for sure this is 100% human authored because the AI doesn’t yet have the kind of brain damage nor mental illness necessary to express what it’s like to trade Euribors in words.

Still, this is Global Macro Trading for Idiots, not “for idiots, by idiots”. And while I can certainly punt midcurves efficiently, I needed someone who understood both memes and STIR well enough to bring this to the next level.

There’s a lot of stuff that’s beyond my realm in terms of IR Swaps, FX Swaps, Cross-Currency Basis etc. that I needed a real expert in…

And then I saw this:

Bingo.

I’m going to take you from “what’s a sofr” to “let’s put on the z4z5 steepener” and he will take you the rest of the way down the rabbit hole with an overview that features such nonsense words as “cross currency basis” and “covered interest rate parity.

It’s going to be really fun…interesting…STIRrific…

Okay, I’m not going to lie to you, you will hate both of us by the end of this article.

But at least you’ll have a solid foundation in short term interest rate trading. Provided that, when it comes to trading STIR, you’d currently self-describe as an idiot or some synonym thereof.

Because that's where "Global Macro Trading for Idiots" comes in.

Just be forewarned that we’ll be getting progressively less idiotic as the article goes on, thanks to the contributions of notorious non-idiot (in matters STIR related) Sir of Finance.

One more thing: normally I split the revenue generated from my articles with my collaborators. This is going out to everyone, free of charge, and because Sir of Finance is a gentleman (as the name infers),

We’ll be donating half of all subscription fees generated through this article to Doctor’s Without Borders. Unfortunately, there was no charity set up ready to accept donations for traders who have brain damage due to trading Euribors.

Upgrade to paid

Okay, with that said, let’s begin…

The (Very) Basics of STIR and STIR Futures

For the uninitiated, STIR futures are derivative contracts that allow traders to bet on the future direction of short-term interest rates, typically tied to interbank lending rates like or central bank policy rates. They're the purest way to express your view on what central bankers will do (or won't do) in the coming months and years. And if you really want to get fancy, you can even trade options on these futures to create all sorts payoff profiles.

But before we get into the nitty-gritty of cross-currency basis, DV01 and midcurves, let's take a step back and understand why anyone would even bother with these instruments in the first place. Since central banks are the puppet masters of the global economy, pulling the strings of interest rates to keep inflation in check or promote growth, macro traders spend pretty much all their time anticipating their next move and position accordingly.

STIR futures provide a liquid and efficient way to do just that. And not just that, but ways to do that with accuracy you just can’t get in other instruments.

If you think the ECB will be forced to cut rates into negative territory by the end of the year, you’re going to want to be doing something with Euribors if that’s the extent of your thesis.

The differential to SOFR won’t matter like it would with EURUSD, and it won’t matter whether it’s a policy mistake that leads to a massive rally in risk assets or it’s response to a previous policy mistake that put the EU in a massive, very-bearish-for-risk-assets recession (for believability the only certainty in this hypothetical is that of an ECB policy mistake).

Regardless of those confounding variables you’d have to deal with by expressing this thesis using other instruments, you’ll make money if you’re long December Euribor Futures (and a lot more money if you’ve got out of the money calls on them).

Maybe you think the market has gotten irrationally exuberant about the quantity of rate cuts the Fed will deliver in 2024? You can sell Z4 SOFR futures. In fact, you can sell some SOFR futures in December 2024 and buy some in December 2025 to isolate your trade to just rate expectations in 2025.

If you think the Bank of Japan will…nevermind actually we’re not going to talk about Japanese rates in this one. (I miss you, Kuroda).

The possibilities are truly (perhaps unfortunately) endless for expressing your unique view on what the economists decide. We’re going to go over some of the basics for doing that, but…

Before we get into it for real, you should be aware that trading STIR futures is not for the faint of heart. These markets are dominated by big banks, hedge funds, and other institutional players with deep pockets. They tend to act a lot differently than other asset classes.

You can go look at how SOFR futures react to headlines and data, unlike trading spoos the reaction in STIR sometimes tends to be much less something that can be described as “price action”. With some degree of regularity, it’s much more accurately described as “teleportation”.

Unlike equity index futures where your win condition is “market participants are currently wrong but eventually see the error of their ways and come around to my way of thinking”, STIR futures have an element of that but also the element of “then a bunch of economists decide whether you’re right or wrong, and sometimes you find out about this decision because one of the economists gets too chatty with the press” and other fun eccentricities.

Here are two examples, post Silicon Valley Bank collapse and the Nikileaks episode of 2022.

Even in significant selloffs in equity indices, there’s some level of liquidity, meanwhile sometimes what you get in STIR is a result that’s so unambiguous (this is the most extreme example of that, since it was literally a WSJ reporter telling the world the Fed would hike 75 and not 50) that between the current price and the correct price there will be zero bids (or zero offers if the scenario was reversed to deal with cuts).

Hence, “teleportation”, as you can see on the above chart showing the reaction of ES vs. SFRM22 to the tweet below from “Fed Whisperer” Nick Timiraos that earned him the nickname among STIR traders of “Nicky Leaks”. Whether that’s an affectionate nickname or one filled with pure hatred is a function of the individual STIR trader’s positioning exactly one second prior to the tweet:

That’s something that you’re going to want to keep in mind when you’re trading and assessing how much risk you’re taking. Obviously if you have a marketable stop order in on a position, you’re going to be facing some level of slippage or generally getting out at worse prices than you could have. If you have a stop order in a SOFR futures position and something like this happens, the only price you’re going to get out at is in the range of the newly-teleported-to correct one.

Now that you’re all sufficiently frightened by them, let’s get into the basics of trading STIR, beginning with how STIR futures work.